Nifty Index Investing Newsletter [23rd Nov 2024]

What to do in current market scenario ? SIP or Lump sum ?

Nifty 50 started the week on negative note, breaching 200 DMA for the first time in more than a year. I’ll repeat, Nifty 50 breached its 200 DMA for the first time in more than a year. Post breach, it gave more worries to all tracking it as it stayed below 200 DMA without any covering or a relief rally to bring it back above 200 DMA. I mean, just see the rally we got on Friday, ~2.4% gain in one single day. This one day boost was enough to lift spirits of people on social media. But tbh, just see the chart below, we are in a downwards channel and this one buying session should not be read much into until this channel is broken on the upside. I have a feel we might stay in this channel, but let’s see what happens in the upcoming week..

Is it overbought/oversold now? Should one buy/sell ? I certainly don’t know, but what we know is how to measure the data points we have been week over week and take decision accordingly as per our risk tolerance. :)

[Please note, I only track 750 stock universe comprising of NIFTY500 and NIFTYMicroCap250 indexes]

Market Breadth is still in redwoods for now. Until stocks above 200 DMA cross 50% benchmark, I would be vary of taking any big positions in the market stock wise, but guess what, for buying indexes and averaging units, this is a good time. Last few weeks have been lumpsum triggers on a series. %Stocks above 21 DMA have improved this week from 17% to 28% so its a huge improvement. I really do hope this gets translated ahead to 50 DMA and 200 DMA in the upcoming weeks. That way what we buy in lumpsum on indexes will show returns and markets will resume its uptrend.

World Markets, notice how I changed this chart with 21 DMA and 50 DMA instead. World markets look solid. they bounced back from 50 DMA and even went above 21 DMA in one week itself. Last week we were talking about if 50 DMA support kicks in for 3rd time in a row, well it did indeed and bounce was strong. Let’s see if we make new highs soon or we retrace to test 50 DMA support again.

But as you know, we are not here to predict what happens, we are here to understand if its time to press on the gas for lumpsum investments or just do our normal SIPs ;)

Let’s get to the meat of this week’s update and see how the Nifty Market Breadth Tables are looking now. Following are the links in case you missed the previous 3 updates :

02nd Nov 2024

09th Nov 2024

16th Nov 2024

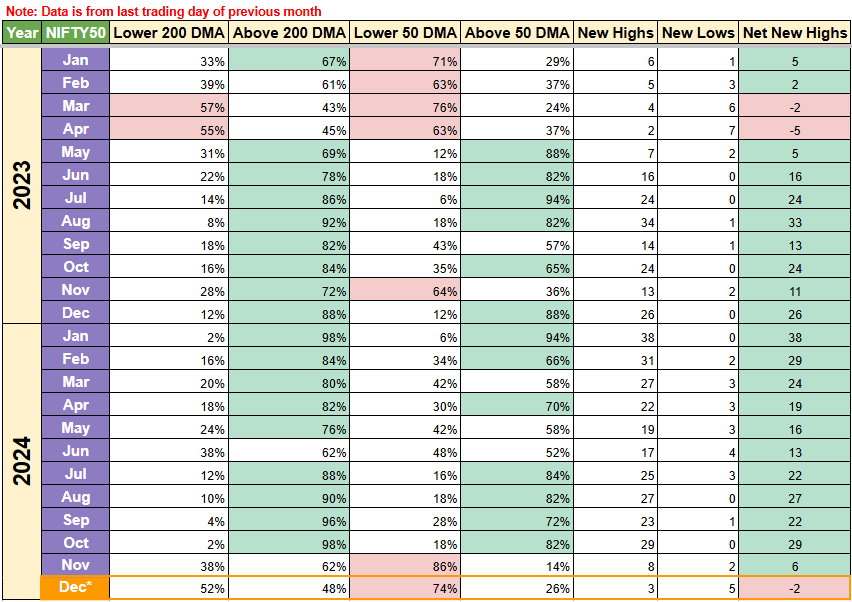

Nifty 50 Breadth has improved w.r.t last week. Well not really a competition as last week was extreme numbers. 90% Stocks below 50 DMA vs 74% now, so we do see some pull back in breadth numbers. I think we should thank the buying on Friday for this mainly. What indicator is tough to move though is net new highs i.e. -2 and since it lags the market, it still shows, Nifty 50 stocks are making more lows than highs. If we get a good upcoming week, this indicator will be the last one to improve and will confirm some sort of a trend that we can read with the numbers.

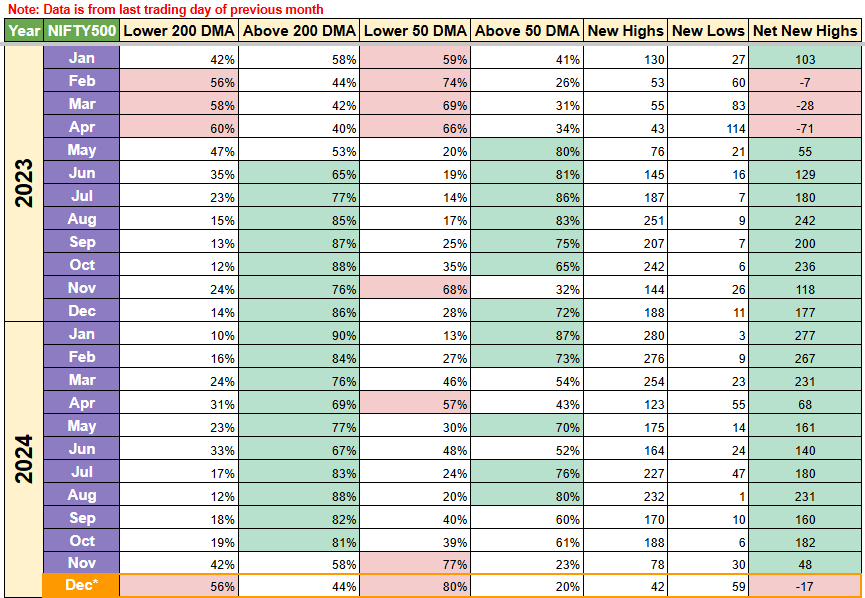

Nifty 500 has not improved much week over week, well not completely true, directionally we have improved but we still have more red here than Nifty50. %Stocks below 50 DMA is not 80% vs 86% last week. Not a significant improvement by any means but can see market being held a bit. Still in lumpsum territory though and net new highs are now in negative territory after a long long time, just see the grid, last time we had this was in March 2023. So markets might be repeating that phase, and this time we can see the numbers showing us that ;)

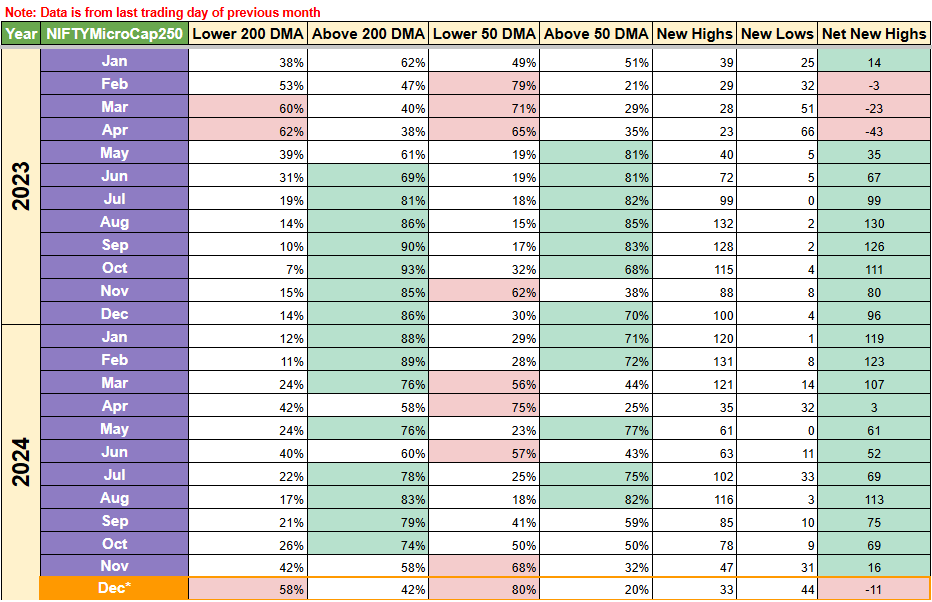

Nifty MicroCap 250 has improved the least week over week. Showing that last week Large caps and midcaps were the ones which had interest and smallcaps and microcaps were just ignored and didn’t participate much. 82% stocks were below 50 DMA last week and now its 80%, so even in directional terms I won’t be reading into it at all. Maybe we are due the most pain in microcaps as per the data. Let’s see how the indexes fair in this game of markets. We have an interesting time ahead :)

Maybe it is a sign of things to come, maybe not. All we can do it read the table week over week and press on that beautiful app on our smartphones to buy more units for our passive investments ;)

[Give it time, these numbers will become second nature once you keep looking at it every week]

So, my fundamental rule here is “red cell in the row” be aggressive and buy lumpsum ELSE keep the monthly SIP rolling as per plan…

Based on the above rule, I’ll be taking the following steps as a summary :

Nifty 50 → Go for Lumpsum units over and above SIP if already done.

Nifty 500 → Go for Lumpsum units over and above SIP if already done.

Nifty MicroCap 250 → Go for Lumpsum units over and above SIP if already done.

As always, I’ll be sharing weekly updates with the above tables and it will slowly become apparent when can one be aggressive or when can one continue with SIPs. As long as data gives comfort to invest big, that’s all we need it for. Removing emotion from SIPs is the best thing a passive investor can do. And investing big lumpsum amounts when the time comes will be like a rocket fuel to overall corpus.

For reference, in 2023, One could have been aggressive with lumpsum investments in Jan-Feb-Mar-Apr-Nov as per data in the above tables. This would have resulted in better returns when we consider investing in the Indexes (whether it be Nifty50, Nifty500 or Nifty MicroCap250).

Intention here is to average out fund units when turbulence hits. This way we lower our average purchase price more aggressively than when done with SIPs.

Please note, this strategy is usable only when one believes the India story and want to be part of India’s growth. If India has to grow and become a bigger economy, then Indexes like Nifty50, Nifty500 & NiftyMicroCap250 have to go much higher from here.

Covering Top 750 stocks (Nifty 500 and NiftyMicroCap250) is more than enough for the passive investor, going beyond that becomes too risky as liquidity is not supportive much.

Have a great week ahead and Happy Investing :)

[Disclaimer: The information in this article is for informational purposes only and is not financial advice. The author is not a licensed financial advisor. Readers should conduct their own research and consult with a qualified professional before making any financial decisions.]